Is Freeport McMoRan (FCX) Still Attractive After A 90% One Year Share Price Surge

Track your investments for FREE[1] with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

-

If you are wondering whether Freeport-McMoRan is still reasonably priced after its strong run, this article will walk you through what the current share price might be implying about value.

-

The stock closed at US£65.57 most recently, with returns of 8.9% over 30 days, 26.3% year to date, and 90.5% over the past year, which can influence how much upside or risk investors feel is left.

-

Recent headlines around Freeport-McMoRan have focused on its role as a major copper producer and how that connects to long term demand themes, as well as ongoing attention on its large scale mining assets and related capital spending. These stories help frame why the share price has moved and what the market could be reacting to.

-

Even after those moves, Freeport-McMoRan currently scores 2 out of 6[2] on our valuation checks. Next, we will look at how different valuation methods line up on the stock, before finishing with one approach that can give you a clearer overall view of value.

Freeport-McMoRan scores just 2/6 on our valuation checks.

See what other red flags we found in the full valuation breakdown[3].

A Discounted Cash Flow, or DCF, model takes estimates of a company's future cash flows and discounts them back to today. It aims to translate those future dollars into a single present value per share.

For Freeport-McMoRan, the model used is a 2 Stage Free Cash Flow to Equity approach, based on its latest twelve month free cash flow of about £678.0 million. Analyst forecasts and extrapolations then extend out over the next decade, with projected free cash flow in 2030 of around £8.6b in £.

The ten year path includes annual projections sourced from analysts for the earlier years and then mechanically extended by Simply Wall St for the later years. This introduces uncertainty but gives a structured way to compare cash flows over time.

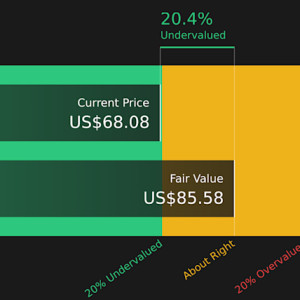

On this basis, the DCF model arrives at an estimated intrinsic value of about £83.90 per share, compared with the recent share price of £65.57. That gap implies the stock is around 21.8% undervalued according to this single method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Freeport-McMoRan is undervalued by 21.8%.

Track this in your watchlist[4] or portfolio[5], or discover 49 more high quality undervalued stocks[6].

FCX Discounted Cash Flow as at Mar 2026

FCX Discounted Cash Flow as at Mar 2026

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Freeport-McMoRan.[7]

For a profitable company like Freeport-McMoRan, the P/E ratio is a useful way to think about valuation because it links what you pay directly to the earnings the business is generating today. Investors usually accept a higher or lower P/E depending on what they expect for future earnings growth and how risky those earnings look.

Freeport-McMoRan is trading on a P/E of 42.89x. That sits above the Metals and Mining industry average P/E of 23.49x and above the peer group average of 26.45x.

On its own, this might suggest the market is paying a higher price for each dollar of earnings compared with many other miners.

Simply Wall St's Fair Ratio tries to refine that comparison. It is an estimate of what P/E you might expect for Freeport-McMoRan after considering factors like its earnings growth profile, industry, profit margins, market cap and risk characteristics. Because it is tailored to the company, it can be more informative than a simple industry or peer comparison.

For Freeport-McMoRan, the Fair Ratio is 34.02x, which is below the current 42.89x P/E and indicates the shares look overvalued on this measure.

Result: OVERVALUED

NYSE:FCX P/E Ratio as at Mar 2026

NYSE:FCX P/E Ratio as at Mar 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies[8].

Earlier we mentioned that there is an even better way to understand valuation.

Let us introduce you to Narratives, which are simple stories investors create on Simply Wall St's Community page that link their view of a company's future revenue, earnings and margins to a fair value. They then compare that fair value with today's share price to frame potential buy or sell decisions. Narratives update automatically as new news or earnings arrive.

For Freeport-McMoRan, one investor might build a more upbeat Narrative around higher revenue growth and a fair value of US£70.00, while another takes a cautious view tied to a fair value of about US£36.50. Both of those stories sit alongside the analyst consensus style view around US£50.48, giving you a clear range of perspectives to measure your own assumptions against.

For Freeport-McMoRan however we will make it really easy for you with previews of two leading Freeport-McMoRan Narratives:

Together, they show how different investors can look at the same set of assets and headlines and still land on very different views of value and risk.

? Freeport-McMoRan Bull Case

Fair value: US£70.00 per share

Implied valuation gap: about 6.3% above the recent US£65.57 share price

Revenue growth assumption: 17.13% a year

-

Builds a case around stronger copper demand, higher assumed revenue growth, and improved profit margins, helped by Freeport-McMoRan's position in large copper assets and progress at Grasberg.

-

Assumes earnings and margins step up over the next few years, with the P/E ratio easing back from current levels to a lower multiple on higher earnings.

-

Flags meaningful risks around jurisdiction, environmental and regulatory pressure, and copper demand shifts, so the bullish outcome still depends on execution and external conditions not breaking the thesis.

?

Freeport-McMoRan Bear Case

Fair value: US£44.08 per share

Implied overvaluation: about 48.7% relative to the recent US£65.57 share price

Revenue growth assumption: 4% a year

-

Highlights an unstable dividend record, cyclicality, and sensitivity to copper prices as key watchpoints for anyone treating Freeport-McMoRan as a long term holding.

-

Sees more modest revenue growth but a quicker lift in earnings, which still leads to a fair value that sits well below the current share price.

-

Recognises long term copper demand drivers from EVs, AI and green infrastructure, along with Grasberg and major U.S. mines, but treats these as already well understood and not enough to offset the risks at today's price.

These two narratives bracket a wide valuation range, from about US£44 to US£70. Where you land inside that band depends on how confident you are about copper demand, Grasberg and other key assets, and how much risk you are willing to accept for Freeport-McMoRan at its current share price.

Curious how numbers become stories that shape markets?

Explore Community Narratives[9]

Do you think there's more to the story for Freeport-McMoRan? Head over to our Community to see what others are saying![10]

NYSE:FCX 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include FCX[11].

Have feedback on this article? Concerned about the content? Get in touch[12] with us directly. Alternatively, email [email protected][13]

References

- ^ Track your investments for FREE (simplywall.st)

- ^ 2 out of 6 (finance.yahoo.com)

- ^ full valuation breakdown (www.simplywall.st)

- ^ watchlist (simplywall.st)

- ^ portfolio (simplywall.st)

- ^ 49 more high quality undervalued stocks (simplywall.st)

- ^ Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Freeport-McMoRan. (www.simplywall.st)

- ^ Start investing in legacies, not executives.

Discover our 18 top founder-led companies

(simplywall.st) - ^ Curious how numbers become stories that shape markets?

Explore Community Narratives

(simplywall.st) - ^ Head over to our Community to see what others are saying! (simplywall.st)

- ^ FCX (finance.yahoo.com)

- ^ Get in touch (investor-research.typeform.com)

- ^ [email protected] (finance.yahoo.com)