Freeport-McMoRan (FCX) Valuation Check After Strong Recent Share Price Momentum

Advertisement

Freeport-McMoRan: recent performance puts copper miner in focus

Freeport-McMoRan (FCX) is drawing investor attention after recent share price moves, with the stock up 1.9% over the past day, 4.3% in the past week, and 8.5% over the past month. See our latest analysis for Freeport-McMoRan.[1] Those recent gains build on a stronger trend, with a 90 day share price return of 59.61% and a 1 year total shareholder return of 79.09%, suggesting momentum has been building over both shorter and longer horizons.

If copper exposure is already on your radar, this could be a good moment to see what else is moving in the space with our 8 top copper producer stocks[2] identified by the Simply Wall St screener. With Freeport McMoRan trading close to its US£65.82 analyst price target, yet showing an estimated 23% intrinsic discount, the key question is whether there is still a buying opportunity here or if markets are already pricing in future growth.

Most Popular Narrative: 48.7% Overvalued

According to the most followed narrative, Freeport McMoRan's fair value sits at £44.08, well below the last close of £65.55, which frames the recent rally in a very different light.

Global demand for copper, especially from EVs, AI, and green infrastructure Grasberg mine in Indonesia and large scale U.S. operations (e.g., Morenci, Bagdad)

U.S. legislation may classify copper as a "critical mineral", possibly introducing 10% tax creditAssumptions

Read the complete narrative.[3] Curious how this view still lands on a lower fair value than today's price? The narrative leans heavily on steady top line growth and improving profitability assumptions over several years, then pairs that with a future earnings multiple that might surprise you.

The tension between those forecasts and the implied return expectations is where the story gets interesting. Result: Fair Value of £44.08 (OVERVALUED) Have a read of the narrative in full and understand what's behind the forecasts.[4]

However, you still need to weigh risks such as copper price swings affecting this highly cyclical business, as well as potential setbacks at large mines such as Grasberg. Find out about the key risks to this Freeport-McMoRan narrative.[5]

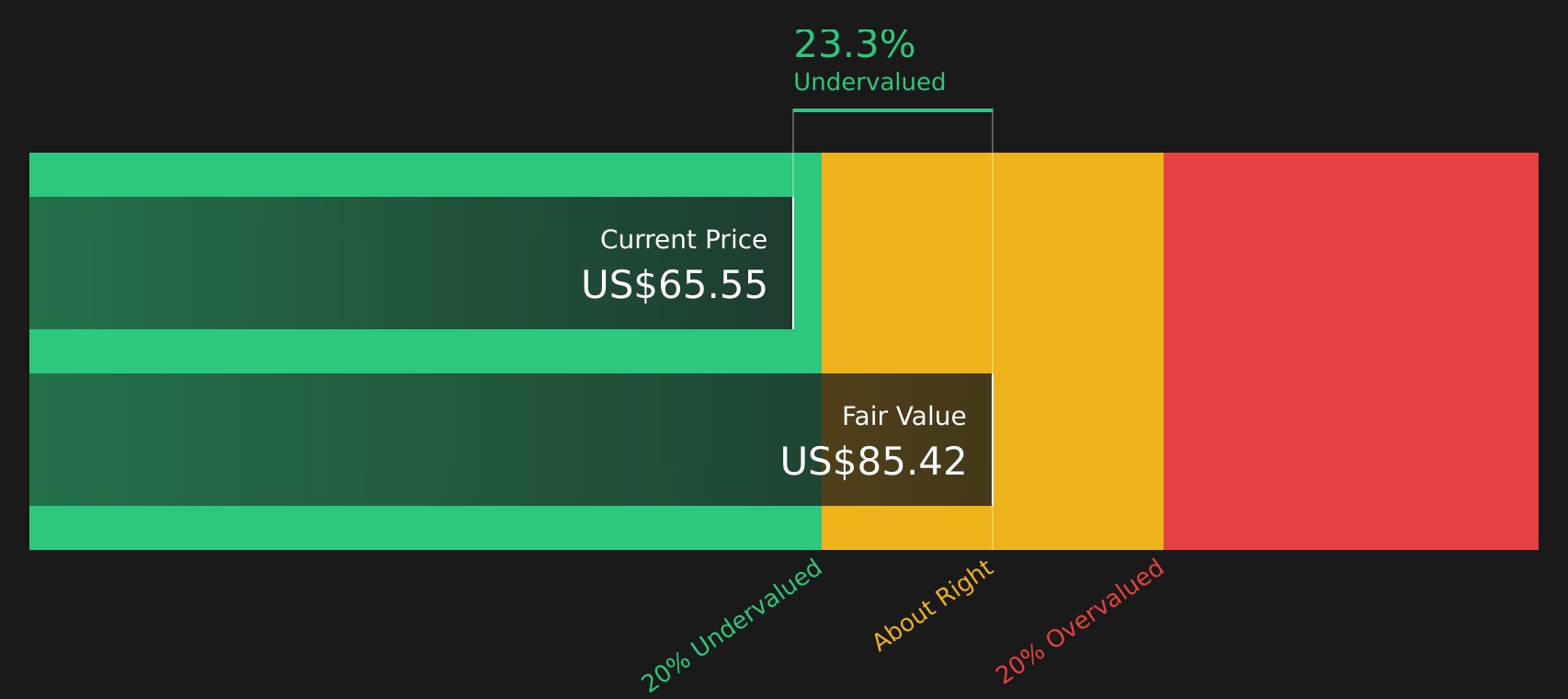

Another angle on value: DCF points the other way

That 48.7% overvalued narrative is not the only story. Our DCF model, which values Freeport McMoRan at £85.42 per share based on its future cash flows, suggests the stock is trading about 23.3% below that estimate at £65.55.

One model says caution; the other hints at a discount. Which set of assumptions feels more realistic to you? Look into how the SWS DCF model arrives at its fair value.[6]

FCX Discounted Cash Flow as at Feb 2026

FCX Discounted Cash Flow as at Feb 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Freeport-McMoRan for example[7]).

We show the entire calculation in full. You can track the result in your watchlist[8] or portfolio[9] and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks[10]. If you save a screener[11] we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of signals seems conflicting to you, it is.

Take a moment to review the key data points, then move quickly to shape your own view with 2 key rewards and 1 important warning sign[12].

Looking for more investment ideas?

If you are serious about sharpening your portfolio, do not stop at one copper name. Use the Simply Wall St screener to surface fresh opportunities fast. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation.

We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

o Dividend Powerhouses (3%+ Yield)

o Undervalued Small Caps with Insider Buying

o High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free[13]Have feedback on this article?

Concerned about the content? Get in touch[14] with us directly. Alternatively, email [email protected][15]

References

- ^ See our latest analysis for Freeport-McMoRan. (www.simplywall.st)

- ^ 8 top copper producer stocks (simplywall.st)

- ^ Read the complete narrative. (www.simplywall.st)

- ^ Have a read of the narrative in full and understand what's behind the forecasts. (www.simplywall.st)

- ^ Find out about the key risks to this Freeport-McMoRan narrative. (www.simplywall.st)

- ^ Look into how the SWS DCF model arrives at its fair value. (www.simplywall.st)

- ^ check out Freeport-McMoRan for example (www.simplywall.st)

- ^ watchlist (simplywall.st)

- ^ portfolio (simplywall.st)

- ^ 56 high quality undervalued stocks (simplywall.st)

- ^ save a screener (simplywall.st)

- ^ 2 key rewards and 1 important warning sign (www.simplywall.st)

- ^ Explore Now for Free (simplywall.st)

- ^ Get in touch (investor-research.typeform.com)

- ^ [email protected] (simplywall.st)